Proteus shortlisted for NFRC Award at 25 Moorgate

Proteus Waterproofing has successfully delivered a highly complex roof waterproofing package at 25...

Read More

Proteus Waterproofing has successfully delivered a highly complex roof waterproofing package at 25...

Read More

Young people giving up on training schemes as the Government struggles to meet new homes target...

Read More

IV PRODUKT ANNOUNCES OFFICIAL UK LAUNCH OF NEXT-GENERATION THERMOCOOLER HP WITH R290 AND R454C...

Read More

For Britain’s prime minister, Andy Burnham, a sprawling car park in the centre of ...

Read More

JCB is stepping up efforts to improve the security and emissions visibility of its Stage V...

Read More

Story Contracting has been served two prohibition notices by the Health and Safety...

Read More

Esholt pioneering 150-home eco village and major biotech employment hub powered by a live sewage...

Read More

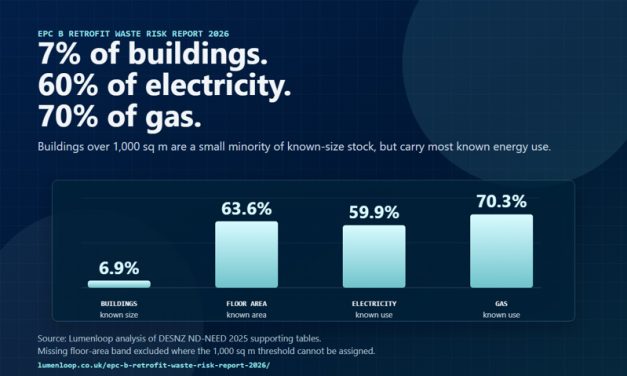

New report says proposed EPC B requirements for larger rented commercial buildings should cut...

Read More

The long-stalled UK Health Security Campus in Harlow has finally moved back towards restarting...

Read More

Northern Trains has launched preliminary market engagement for a planned £300m framework covering...

Read More